Asia Insights: Seeking Stable Returns

Introduction

Aaron Costello, Regional Head for Asia, and Vivian Gan, Associate Investment Director, Capital Markets Research

With the global economy showing signs of cooling and Chinese economic momentum remaining weak, the outlook for Asian markets is increasingly mixed. Certain markets have been more resilient, such as India, where domestic growth is still robust, and Taiwan, which has benefitted from the global rally in semiconductor and artificial intelligence (AI)–related stocks. However, elevated valuations in these segments pose a concern for investors, prompting a reassessment of opportunities elsewhere. In the current environment, a rotation towards markets that may be more defensive and where shifts in market dynamics are supportive of longer-term prospects is warranted. In this edition of Asia Insights, we highlight:

- Within Asia Public Equities, there is a growing emphasis on shareholder returns and a rise in the number of companies increasing dividend payouts and initiating share buybacks. This trend comes amid a market rotation towards high dividend–yielding companies, as investors seek stable income returns given rising uncertainty and overvaluations in certain segments of the market.

- In Asia Private Credit, capital has rotated away from China and towards developed markets such as Australia and South Korea, while India also remains a destination for capital. Broadly, the Asia private credit market remains underpenetrated and is less crowded but poised for growth, presenting an interesting opportunity for investors to gain a diversified exposure.

- India Venture Capital (VC) is also starting to look more attractive today given a favourable macroeconomic backdrop, an improving start-up and manager landscapes, and a broadening of exit channels. In contrast to India public markets, which have run up and appear frothy, India VC activity has cooled alongside global VC markets. As a result, India VC valuations are moderating, making now a more opportune time for investors considering access.

- Across China Private Investments, fundraising activity remains frozen given uncertainty over geopolitical tensions and pending US investment restrictions. However, deal-level opportunities still exist in certain segments of the market, particularly for buyouts where the current macro environment is conducive for market consolidation and control opportunities.

Asian Public Equities: A New Era for Shareholder Returns

Wilson Chen, Managing Director, Public Equities

In Asia, we have seen an increased emphasis on shareholder returns and a notable rise in the number of companies initiating share buybacks and increasing dividend payouts. Japan, driven by regulatory changes and increased shareholder activism, has led this shift. Reforms introduced by the Tokyo Stock Exchange in January 2023 have put pressure on Japanese companies that trade below book value to take action to narrow their valuation discount, largely through increasing dividends and conducting shares repurchases. Such measures have helped to boost Japanese companies’ return-on-equity and supported upward stock price revaluations, creating positive tailwinds for the market. The small-cap segment could see greater benefits from reforms, given wider valuation discounts.

In South Korea and China, similar efforts are now being observed. South Korea’s ‘Corporate Value-up Program’ seeks to improve capital efficiency and equity valuations of firms through the voluntary disclosure of plans to enhance shareholder value. In China, more firms are responding to regulatory calls to increase dividends and share buybacks and others are re-listing on more favourable exchanges or spinning off units to unlock value and boost investor confidence.

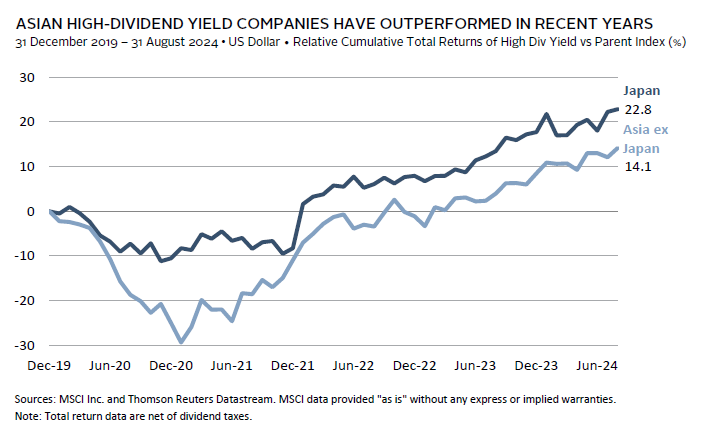

From a total return perspective, dividends have always played a crucial role, although their importance has been magnified in markets such as China, which has seen weaker earnings growth and depressed valuation multiples. In the current environment, investors have rewarded companies able to generate high, stable income returns, a rotation that is reflected in the performance of the MSCI AC Asia ex Japan High Dividend Yield Index, which has outperformed its parent index by 4.2 percentage points (ppts) year-to-date and 9.4 ppts over the trailing one year. The trend of increased emphasis on shareholder returns in Asia is positive for investors and may also be a more defensive strategy given rising uncertainty and overvaluations in certain segments of the market, such as semiconductors and AI-related stocks.

Asia Private Credit: Growing Momentum for Asia ex China Strategies

Vijay Padmanabhan, Managing Director, Credit Investments

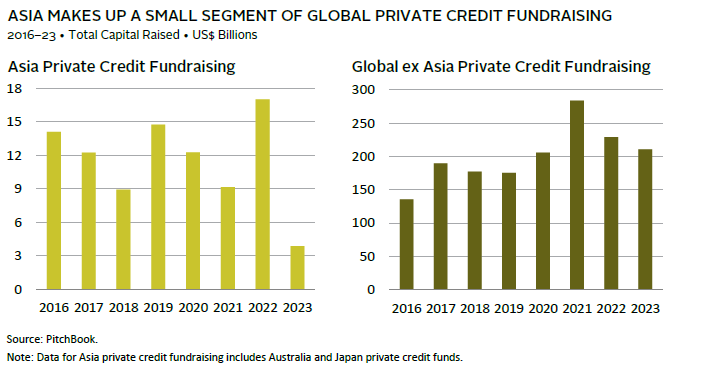

Private credit in Asia (including Japan and Australia) remains an underpenetrated market relative to the size of the region’s economy and demand for capital. Private credit and other forms of non-bank credit represent approximately 20% of the total Asia credit market, as compared to 65% in North America. Meanwhile, fundraising by Asia-based private credit funds amounted to just 5% of total capital raised by global private credit funds in the trailing five years ending 2023.

Fundraising activity slowed sharply in 2023, with lacklustre activity in part due to ongoing weakness in China’s property market. Many pan-Asian general partners had been overweight China prior to its real estate crisis, and the performance of these strategies, as well as that of dedicated China funds, has continued to struggle since.

Outside of China, however, the opportunity set remains robust. Managers are increasingly pivoting to developed Asia markets such as Australia and South Korea, which are credit-friendly jurisdictions in which banks are retrenching and high-quality collateral is available. The presence of higher sponsor activity in these markets creates space for sponsor-backed lending opportunities, while credit opportunities in sectors such as real estate are also rising given a trend of tightening liquidity from traditional lenders. Across emerging Asia, India is a bright spot for managers given its resilient economic growth outlook and improving credit regulations and credit landscape. India private credit had predominantly leaned towards distressed credit due to its legacy non-performing asset challenges and, more recently, in the aftermath of its NBFC (non-bank financial company) liquidity crisis. However, the strategies have since broadened to include performing credits in the underserved, midmarket segment, and solution capital to businesses for share buybacks and growth or acquisition financing.

Lower penetration and competition today create a compelling environment for Asia private credit strategies, as these allow for deals to be executed at better terms, pricing, and covenants. Overall, the market is poised for growth and presents an interesting opportunity for investors seeking to gain a diversified exposure across both developed and emerging Asian credit markets.

India Private Investments: The Growing Attractiveness of India Venture Capital

Vish Ramaswami, Head of Asia-Pacific Private Investments and Sharad Todi, Senior Investment Director, Private Equity

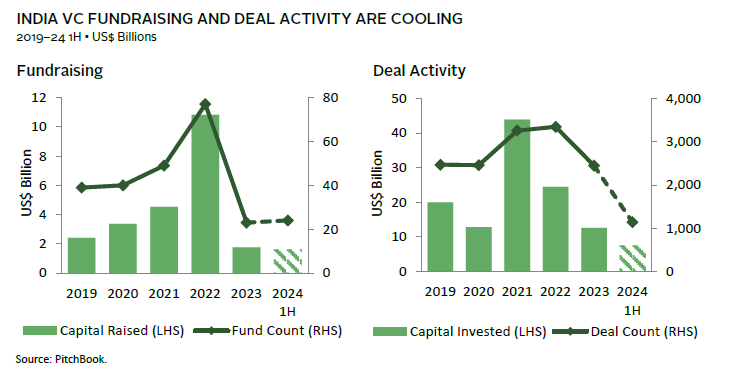

Amid a mixed economic outlook for Asia, India has stood out for its resilient economic growth. As a result, India public equity markets have run up and appear frothy, making some investors cautious about entering the market. In contrast, India’s VC market is cooling in terms of fundraising and deal activity alongside a shakeout in global VC markets, and valuations have moderated, particularly for later-stage VC. Given India’s long-term growth potential and favourable government policies, today may be a more attractive entry point for India VC in our view.

Dedicated India VC fundraising totaled only $1.8B in 2023, down sharply from more than $10B in 2022, and remains small compared to total global VC fundraising at $201B. Yet, India VC is benefitting from an improving start-up landscape in terms of the quality of founders, business models, and technology. The Indian government has spearheaded the creation of a digital public infrastructure or ‘India stack’, which has been widely adopted by start-ups to create disruptive new business models and tools. Consumer focused start-ups have moved away from cash-guzzling business models and towards profitable, sustainable growth. Enterprise technology start-ups are setting global standards in sectors such as software-as-a-service and financial technology.

Meanwhile, the manager pool has matured significantly. Progressing from a generalist mindset, managers are taking distinct market positions and have developed capabilities beyond simply sourcing deals to enhancing value and risk management. While India VC fund distributions have lagged their global counterparts, this may improve going forward as India’s capital markets broaden. In addition to initial public offerings, new exit routes are emerging, including merger & acquisitions deals and sales to financial sponsors and large family offices.

India VC also provides a different sector exposure compared to Indian public markets, which may be more reflective of the future growth drivers of the Indian economy. Given a cooling of the market, now may be a better time for investors to refresh their assessment of India VC for potential opportunities to gain access.

Chinese Private Investments: Frozen Fundraising, but Deal-Level Opportunities Remain

Vish Ramaswami, Head of Asia-Pacific Private Investments, Scolet Ma, Senior Investment Director, Private Equity, and Linlin Zeng, Investment Director, Private Equity

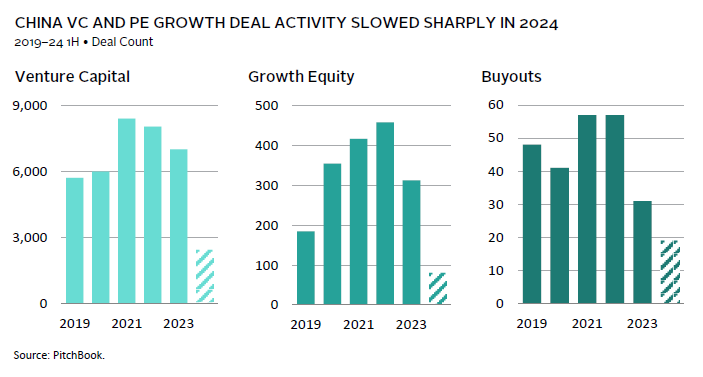

Fundraising for Chinese private equity and venture capital (PE/VC) slowed further in first half 2024 from the already depressed levels seen in 2023. Total capital raised by USD-denominated Chinese PE/VC funds fell to $1.0 billion in first half 2024, down from $16.9 billion in 2023 and $30.1 billion in 2022. Muted levels of fundraising largely reflect uncertainty over geopolitical tensions and pending US investment restrictions on China, although investor sentiments have also been buffeted by a weaker outlook for China’s economic growth and public markets.

Slowing economic momentum and a poor environment for exits have also weighed on VC and growth equity deal activity and exits, particularly for sectors, such as semiconductors and AI, that are subject to pending US investment restrictions. However, pockets of opportunity remain. Healthcare and biotech, for instance, have seen continued foreign investor activity even in the face of the proposed US BIOSECURE Act 1 . A rise in the development of innovative drugs and devices from China has spurred an increase in out-licensing activities and acquisitions by global pharmaceutical companies. Across other sectors, opportunities are similarly present, particularly given some recent downward valuation adjustments. Limited partners that possess a longer investment horizon (i.e., beyond a typical PE/VC fund life of ten years) and have the patience and ability to tolerate uncertainty may be able to take on certain co-investments to capitalize on current attractive valuations.

Meanwhile, Chinese buyout activity picked up in first half 2024, with 19 deals completed as compared to 31 in all of 2023. The current macro environment bodes well for market consolidation and control opportunities. Weaker economic growth in China has created more willing sellers across both domestic founders, as well as multinationals looking to divest from China. Valuation gaps between buyers and sellers have narrowed, and lower borrowing costs in China imply availability of leverage. Although the Chinese buyout market remains less proven, the current environment is favourable in supporting the building out of such strategies.

Derek Yam also contributed to this publication.

Footnotes

- The pending US BIOSECURE Act identifies five Chinese biotech companies that would be prohibited from obtaining US government contracts or deriving revenue from US companies and agencies that receive US government funding. The proposed guidelines do not impose restrictions on US PE/VC investments into Chinese biotech.

About Cambridge Associates

Cambridge Associates is a global investment firm with 50+ years of institutional investing experience. The firm aims to help pension plans, endowments & foundations, healthcare systems, and private clients implement and manage custom investment portfolios that generate outperformance and maximize their impact on the world. Cambridge Associates delivers a range of services, including outsourced CIO, non-discretionary portfolio management, staff extension and alternative asset class mandates. Contact us today.